CEO@TFY. Fintech, Strategy and Business Transformation Expert. Professor at ZIGURAT Institute of Technology.

Blog / Disruptive Technologies

Digital Banking and Neobanks: The Future of Financial Services

Categories

In an era where technology is revolutionising every industry, the financial services sector is no exception.

This article delves into the rise and impact of digital banking and neobanks, exploring how these innovations are reshaping the landscape of financial services and legacy financial institutions.

As a professional with years of experience in fintech and digital transformation, I have witnessed firsthand the evolution of banking from brick-and-mortar institutions to seamless, digital-first platforms that cater to the needs of modern consumers.

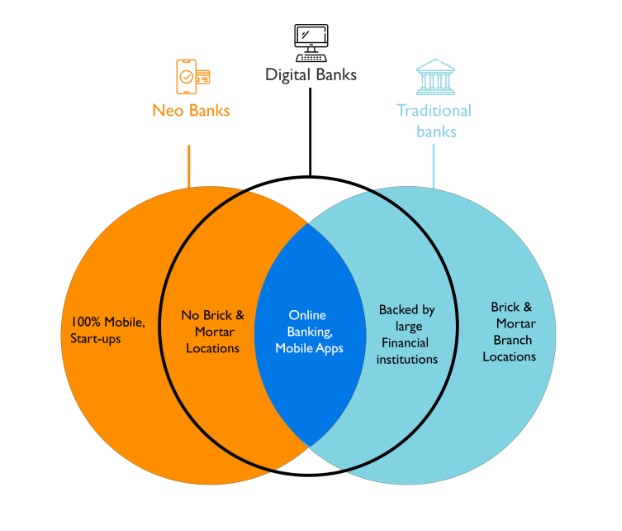

What is Digital Banking?

Digital banking refers to the digitisation of all traditional banking activities and programmes that historically were only available to customers when physically visiting a bank branch. This includes services such as money deposits, withdrawals, and transfers, checking/savings account management, applying for financial products, loan management, and more.

The evolution from traditional banking to digital platforms and neobanks has been driven by the increasing demand for convenience, accessibility, and efficiency. Key features of digital banking include 24/7 access, mobile banking apps, seamless onboarding and know-your-customer (KYC) checks, online transactions, and automated customer service, all of which are designed to offer customers an enhanced and more personalised banking experience.

Understanding Neobanks

Neobanks are digital-only banks that operate without any physical branches, offering a range of financial services through online platforms and mobile apps. Unlike traditional banks, neobanks do not have physical branches, allowing them to operate with lower overhead costs and offer more competitive rates and fees.

Typically, neobanks provide services such as checking and savings accounts, personal finance management tools, cross-border payments, foreign exchange transactions, and even investment products. The fully digital nature of neobanks translates into benefits like lower fees, a user-friendly experience, and innovative features such as real-time spending notifications, budgeting tools, and seamless integration with other financial apps.

Advantages of Digital Banking and Neobanks

Digital banking and neobanks offer numerous advantages over traditional banking, making them increasingly popular among consumers and businesses alike:

- Convenience and Accessibility: With 24/7 access via mobile and online platforms, customers can manage their finances anytime and anywhere.

- Cost-Effectiveness: Lower operational costs often translate to reduced fees and better foreign exchange rates for businesses and consumers.

- Enhanced User Experience: Intuitive interfaces, quick transactions, and real-time notifications create a smooth and enjoyable banking experience. For businesses, the ability to integrate via API with neobanks translates to full automation of payment transactions and foreign exchange operations while handling hundreds of thousands of transactions without human intervention.

- Personalization and Smart Features: Advanced analytics and AI-driven insights allow digital banks to offer personalised financial advice, spending analysis, and budgeting tools.

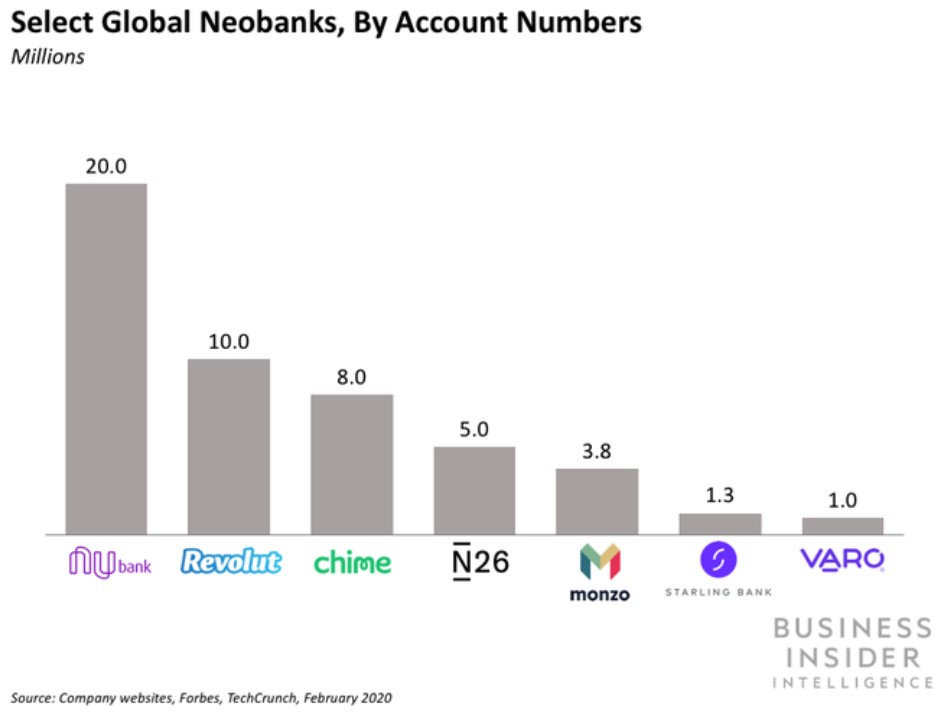

Digital Banking and Neobanks: The Top Players

Several key players have emerged as leaders in the digital banking and neobank space. These include:

- Chime: A U.S.-based neobank known for its fee-free banking services and early direct deposit features.

- Revolut: A UK-based fintech offering banking services, including currency exchange, multi-currency debit cards, crypto and stock trading. The advanced API of Revolut allows fast-growing clients like Transformify(TFY) to handle thousands of payment transactions and big payment volumes without human intervention or the need to hire more people.

- N26: A German neobank with a strong presence across Europe, known for its sleek app and transparent fees.

- Monzo: Another UK-based neobank, popular for its budgeting features and real-time spending notifications.

- Ally Bank: An online-only bank in the U.S. that offers a full range of banking services, including high-yield savings accounts.

Digital Banking: Challenges and Considerations

While digital banking and neobanks offer numerous advantages, they also face several challenges:

- Regulatory Compliance: Navigating complex financial regulations across different regions can be challenging for digital banks, especially as they expand globally. It took Revolut years to obtain a banking license in the UK and its rivals face similar regulatory challenges.

- Security and Privacy Concerns: Protecting customer data and ensuring the security of digital transactions are critical, as cyber threats continue to evolve. Some more conservative users are still reluctant to use mobile banking over fear of their mobile phones being lost or stolen.

- Building Customer Trust: Establishing trust without physical branches requires digital banks to invest heavily in customer support, transparency, and secure technology. Although most users are very happy with support over chat, some urgent matters require telephone support and not all neobanks provide it. As neobanks aim to optimise their costs to the maximum extent possible, there are reported cases of frozen user accounts due to ‘’ fake positives’’ arising from imperfect fraud prevention algorithms, etc.

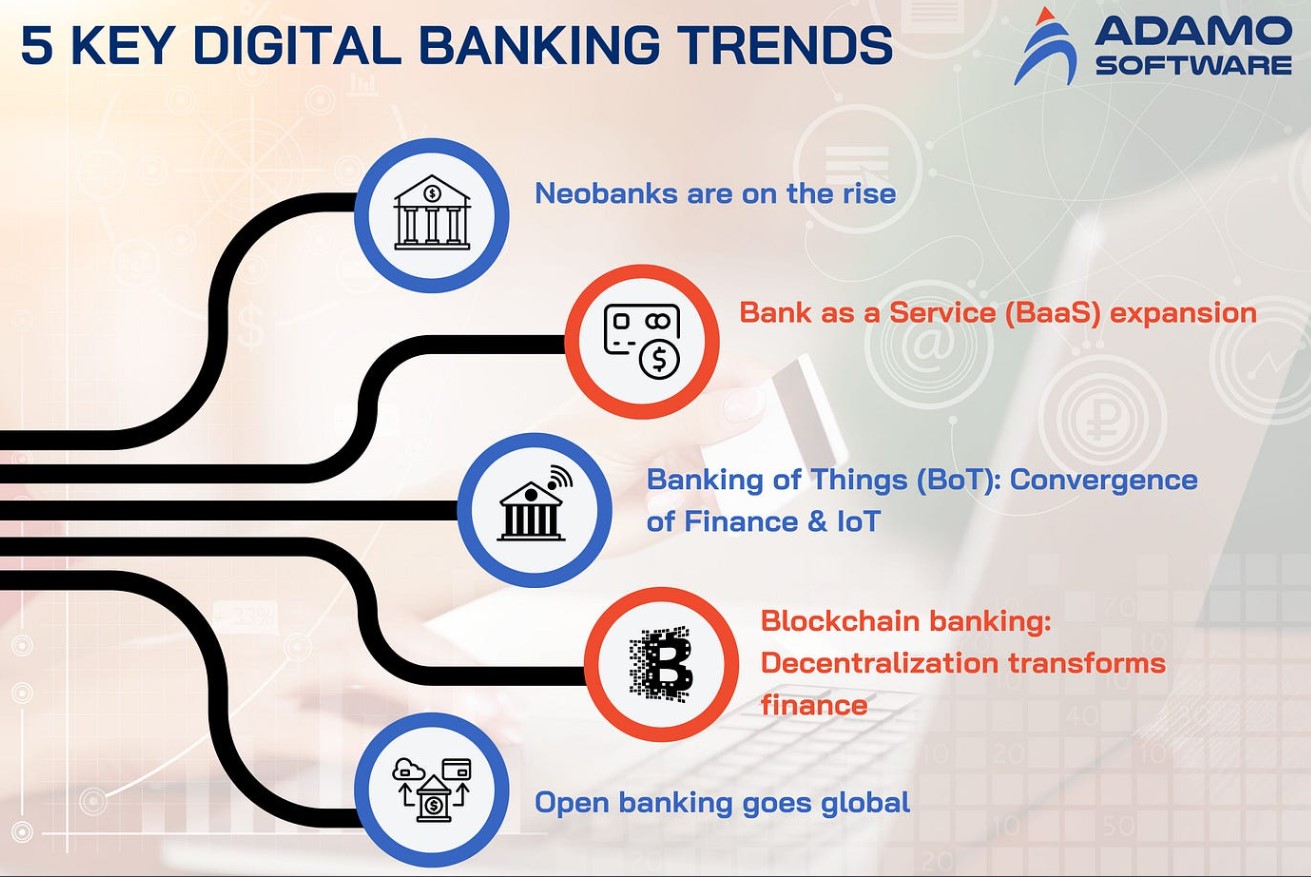

The Future of Digital Banking and Neobanks

The future of digital banking and neobanks looks promising, with several trends set to shape the industry. Emerging technologies such as AI, blockchain, and open banking are expected to drive further innovation, leading to even more personalised and efficient banking experiences. Still, there is a long way to go as many consumers across the globe live in areas with unstable or limited Internet connection or can’t afford mobile devices powerful enough to support banking apps.

As traditional banks face increasing competition from these digital-first challengers, we can expect to see more partnerships, acquisitions, and a continued push towards a fully digital financial ecosystem. The latest M&A and fundraising transactions illustrate this trend including Uruguay-headquartered Prometeo that received in Jan 2024 USD13 million in fresh backing from existing and new investors, including PayPal and Samsung, Nubank’s valuation of USD 44 bn and projected annual profits of USD 1 billion in 2024 and the fundraising ambitions of German neobank N26 and French banking app Lydia. As neobanks struggle to achieve year-on-year growth and user acquisition costs continue to rise, M&A is the obvious growth strategy for many. According to Statista, Neobanking market is projected to reach US$6.37tn in 2024.

Of course, there are risks associated with market consolidation and unsuccessful post-merger integration that may lead to losing customer’s trust.

The impact of these strategic M&A transactions will likely lead to a more integrated, customer-centric approach to banking, benefiting consumers and businesses worldwide.